Wall Street did not buy crypto’s ideology, but it is buying tokenized yield, familiar legal structures, and programmable settlement — and that is how institutional capital actually moves on-chain.

For most of the last decade, crypto tried to recruit institutions with a sermon. The pitch was that finance should be open, disintermediated, composable, and native to blockchain rails. That language inspired builders. It did not persuade pension committees, insurance CIOs, or conservative wealth platforms. Institutions move when a product fits the vocabulary they already use: **yield, duration, custody, legal enforceability, reporting, collateral, and compliance**.

That is why so much of crypto’s first institutional outreach stalled. It was asking allocators to adopt a worldview before adopting a workflow.

Real-world asset tokenization is succeeding because it flips that sequence. It does not begin with ideology. It begins with an asset an institution already understands — a Treasury fund, a money market exposure, private credit, real estate cash flow — and then improves the operating rails underneath it. The point is not to persuade a risk committee to become “crypto-native.” The point is to make a familiar instrument more portable, programmable, and operationally efficient without demanding a leap of faith.

You can already see the evidence in the market’s most credible launches. BlackRock’s BUIDL fund, introduced with Securitize, was positioned around a straightforward institutional proposition: a tokenized product backed by short-term U.S. Treasuries, repurchase agreements, and cash, rather than a speculative invitation to join a subculture.[1] [2] Franklin Templeton’s on-chain government money fund follows the same pattern. Its digital-assets materials state plainly that one BENJI token represents one share of the Franklin OnChain U.S. Government Money Fund, while the fund itself invests at least 99.5% of assets in U.S. government securities, cash, and fully collateralized repos.[3] [4] In other words, the hook is not rebellion. The hook is **operational familiarity with a better wrapper**.

That distinction is the whole story. Crypto’s earlier pitch to Wall Street was, “Come to DeFi because the system is new.” RWA tokenization says, “Come on-chain because the asset is familiar and the plumbing is better.” One message threatens institutional process. The other upgrades it.

Official-sector analysis is increasingly catching up to this reality. The Bank for International Settlements has argued that token arrangements can alter market structure and reshape how money and assets function on programmable platforms.[5] The IMF has gone further, describing tokenization as more than a marginal efficiency gain; in its recent work on tokenized finance, it frames tokenization as a structural shift in financial architecture.[6] Another IMF note on tokenization and financial market inefficiencies emphasizes the potential to reduce frictions that plague today’s market infrastructure.[7] When institutions hear that language from the BIS and IMF, the conversation changes. Tokenization no longer sounds like a fringe experiment. It starts to look like modernization.

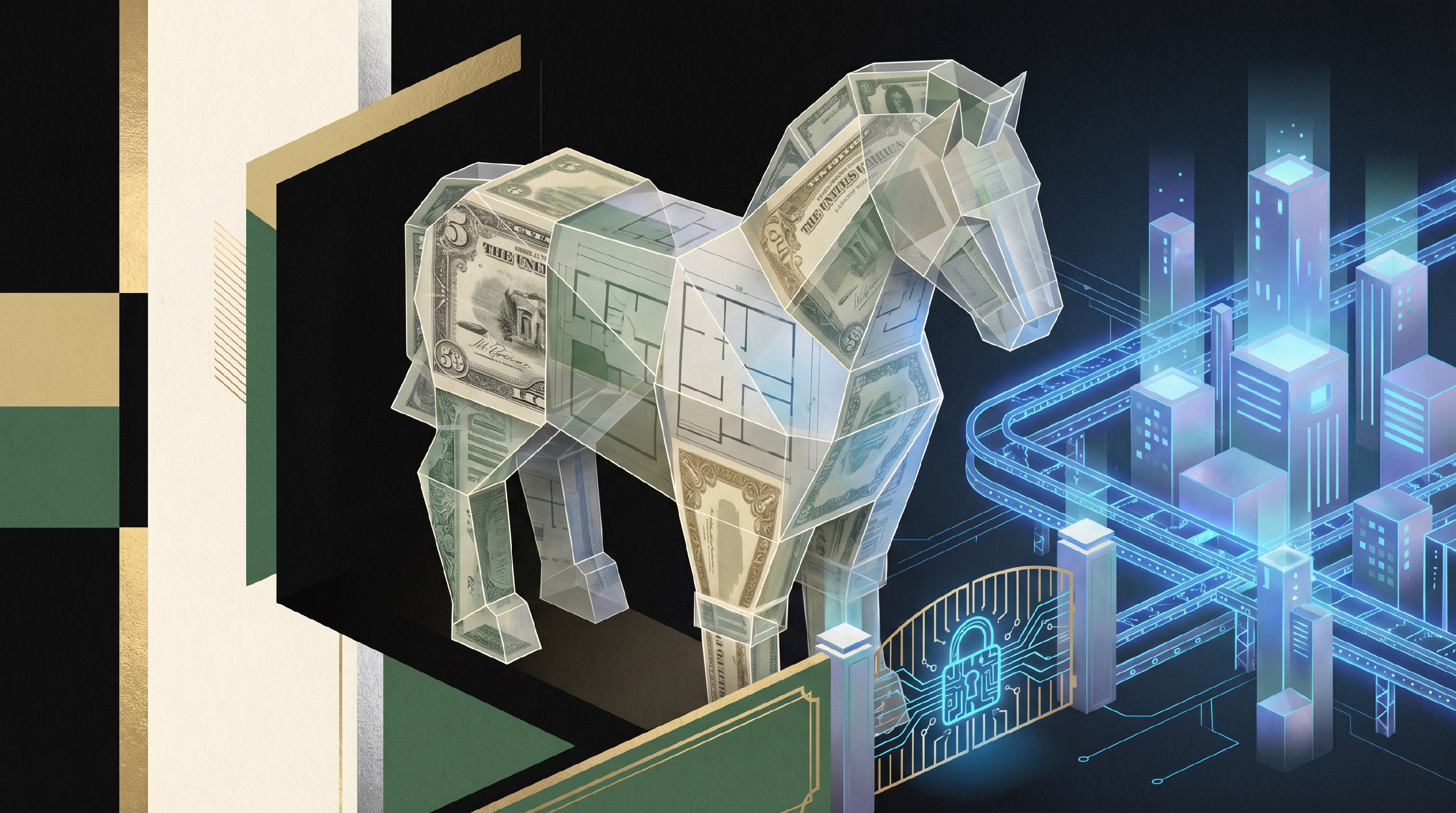

This is why tokenized real-world assets are the Trojan horse for institutional adoption. Once an institution holds a tokenized Treasury exposure in a compliant environment, much of the groundwork has already been done. The institution has approved wallet infrastructure. Its legal, operations, and compliance teams have adapted to ownership, transfer, settlement, reporting, and custody questions. Its investment committee has crossed the psychological threshold that used to separate “real assets” from “digital assets.”

After that, the move into adjacent on-chain products becomes much smaller than the headlines suggest. A pension fund that can hold a tokenized T-bill is no longer debating whether blockchains are unserious. It is debating which on-chain products fit its mandate. From there, the step toward tokenized repo, private credit distributions, on-chain collateral management, or eventually structured lending and derivatives exposure is incremental rather than revolutionary.

This is where so many people still misunderstand the adoption curve. They think institutions arrive in crypto when they buy Bitcoin, allocate to a venture fund, or announce a DeFi strategy. In reality, they arrive much earlier — the moment they accept **blockchain rails as legitimate infrastructure for a traditional financial claim**. That is what RWA tokenization delivers. It normalizes the rails before it normalizes the full product spectrum.

At **BlockStreet.money**, this is the transition we are building for. The opportunity is not to wait for traditional finance to become culturally crypto. The opportunity is to provide the infrastructure that allows traditional capital to move onto programmable rails without losing the controls institutions require. That means translating between on-chain settlement and off-chain fiduciary duties, between programmable assets and real compliance workflows, between token mobility and institutional-grade reporting. The firms that win will not be the loudest evangelists. They will be the best translators.

Crypto spent years trying to persuade Wall Street to come to decentralization on crypto’s terms. That campaign mostly failed. But tokenized real-world assets are doing something more powerful: they are bringing Wall Street on-chain through assets that feel boring, compliant, yield-bearing, and legible to existing allocators. Once that happens, every next step starts to look like a small operational extension rather than a civilizational rupture.

That is why tokenized Treasuries, real estate, and private credit are not just another sector inside digital assets. They are the staging ground for the next institutional market structure.

The institutions are not coming to crypto. **Crypto is going to them, wrapped in a compliance layer they cannot refuse.

Offer Your Reading of What Comes Next. Submit your KOL post today